29 December 2025 | Monday | Analysis

The world of financial services is rapidly being reshaped by technology. By 2026, the global fintech market is expected to exceed $1 trillion and continue growing at double‑digit rates. In just a few years, digital payments and embedded services have flipped the script on cash and cards, while mobile banking and fintech apps have become ubiquitous. Against this backdrop, 2026 looks set to be defined by a convergence of cutting‑edge technologies (AI/ML, blockchain, real‑time networks), bold new business models (neobanks, BNPL, DeFi), and stricter regulation – all combining to make finance faster, smarter and more inclusive. In the following sections, we examine 26 key trends and predictions, explaining what each is, why it matters, and how it is expected to evolve by 2026, with examples and data to illustrate the trajectory.

Artificial intelligence (AI) and machine learning (ML) are no longer futuristic buzzwords – they are already powering core functions in banks, insurers and fintechs. In 2026, AI/ML will underpin everything from risk management to customer service. For example, machine‑learning models can scour transaction data to detect fraud patterns or credit risks far more effectively than rule‑based systems. Banks report that AI usage has moved well beyond pilots: roughly 43% of banks were already using AI for internal functions like risk and fraud by late 2025 (versus only 9% using it in customer‑facing channels), highlighting its role as operational infrastructure rather than a gimmick. Meanwhile, generative AI and “agentic” systems – virtual assistants that can autonomously execute tasks – are emerging. Large banks are piloting AI agents that can automatically process loan applications, approve compliance checks, or even manage trading strategies, further increasing efficiency and speed.

Why it matters: AI allows financial firms to make better decisions faster. By 2026, nearly every bank and insurer will use AI/ML for analytics, forecasting, customer recommendations and automated operations. According to research, the market for AI in fintech is growing explosively (expected to reach roughly $26.7 billion by 2026 with a CAGR ~23%). Firms that leverage AI effectively can detect fraud and money‑laundering much earlier (studies show AI can cut fraud investigation workloads by 20%) , and offer ultra‑personalised advice to customers. For example, banks will increasingly use AI to analyze a person’s spending and income to deliver tailored savings tips or loan offers automatically. In short, AI will evolve from novelty to necessity – enabling hyper‑personalisation (offering the right product to the right customer at the right time) and AI‑driven automation of back‑office processes. By 2026, even routine finance jobs will use AI assistants, freeing humans for strategic work and oversight.

Blockchain technology and cryptocurrencies continue to mature. By 2026 we expect faster, more regulated, and more integrated digital assets. Blockchain – the distributed ledger technology behind Bitcoin and other tokens – is finding real use cases in finance: for instance, banks are using blockchains for faster settlements of securities and cross‑border payments. Meanwhile the cryptocurrency market is growing in scale. In 2024 global crypto market capitalisation surpassed $2.6 trillion. Major players are expanding crypto offerings: PayPal now lets users send crypto internationally, and traditional asset managers are testing tokenised bonds on blockchains.

Why it matters: Cryptocurrencies and blockchain can drastically lower transaction costs and speed up processes, potentially bypassing legacy systems. However, unregulated crypto also poses risks – price volatility and fraud have plagued retail investors. 2026 is likely to see a balance: regulators worldwide are moving from hostility to cautious support. For example, the EU’s MiCA regulation came into effect in 2024 (fully regulating issuers of cryptoassets), and the UK is actively aiming to become a “crypto hub”. Clear rules are emerging, which in turn will boost confidence in using crypto for everyday finance. We expect more financial institutions to adopt digital assets in a controlled way (for example as collateral or for hedging), while retail use will remain primarily speculative. In this regime, “crypto evolution” means better legal frameworks and integration with banks: stablecoins and tokens could be used behind the scenes even if users never see them, for faster settlement and global trade finance.

Stablecoins – cryptocurrencies pegged to fiat currencies – are on track to become a mainstream part of the financial infrastructure. Already, stablecoins like USDC and USDT are being used for B2B settlements and even consumer transfers. In H1 2025 alone, stablecoins processed $8.9 trillion in transactions, with some forecasts projecting the stablecoin market to reach $500–750 billion in the next few years. Unlike volatile cryptocurrencies, stablecoins aim to combine crypto’s speed with the stability of dollars or euros.

Why it matters: By 2026 stablecoins could revolutionise payments. Big tech and fintech firms (and even payment giants like Visa/Mastercard) are exploring stablecoins for instant cross‑border transfers. For example, JP Morgan has estimated that stablecoin transaction volumes already exceed traditional card networks. If regulators clarify rules around reserves and issuance, businesses will trust stablecoins for high‑value transactions. The result: near‑instant, 24/7 settlement across borders at low cost. In practice, this will allow a multinational to move working capital between subsidiaries around the world within seconds, or enable consumers in developing markets to receive digital remittances faster. By 2026 we expect stablecoins to operate under clear compliance frameworks (possibly with reserve requirements), making them a credible tool for commerce, rather than just investment.

Decentralized finance (DeFi) – financial services running on blockchain without central intermediaries – is gaining traction beyond niche crypto circles. DeFi products (like on‑chain lending, decentralized exchanges, and algorithmic stablecoins) are innovating how credit and markets work. Alongside DeFi is the broader trend of tokenization: converting traditional assets (bonds, funds, real estate) into digital tokens on a blockchain. In 2025 the total value of tokenized real‑world assets (RWA) was about $24 billion, with some forecasts suggesting the RWA market could reach $16 trillion by 2030. Early tokenization efforts focus on familiar assets (e.g. corporate bonds or money market funds), reducing frictions in settlement and increasing liquidity.

Why it matters: By 2026 DeFi and tokenization could unlock new markets. Tokenization allows fractional ownership and 24/7 trading of assets that used to require huge investments or slow legacy processes. For example, a large pension fund could issue a tokenized version of a bond portfolio, enabling smaller investors to buy slices that were previously out of reach. This improves market efficiency and inclusion. DeFi itself offers on‑chain lending and borrowing without banks: borrowers can lock crypto collateral to get instant loans, and lenders can earn interest via smart contracts. We expect institutions to adopt “permissioned” DeFi platforms (with regulatory oversight) and for major financial players to build tokenized products. By 2026, aspects of DeFi and tokenization will start to appear in mainstream finance – as an embedded part of trading platforms and wealth management, rather than purely a crypto hobby.

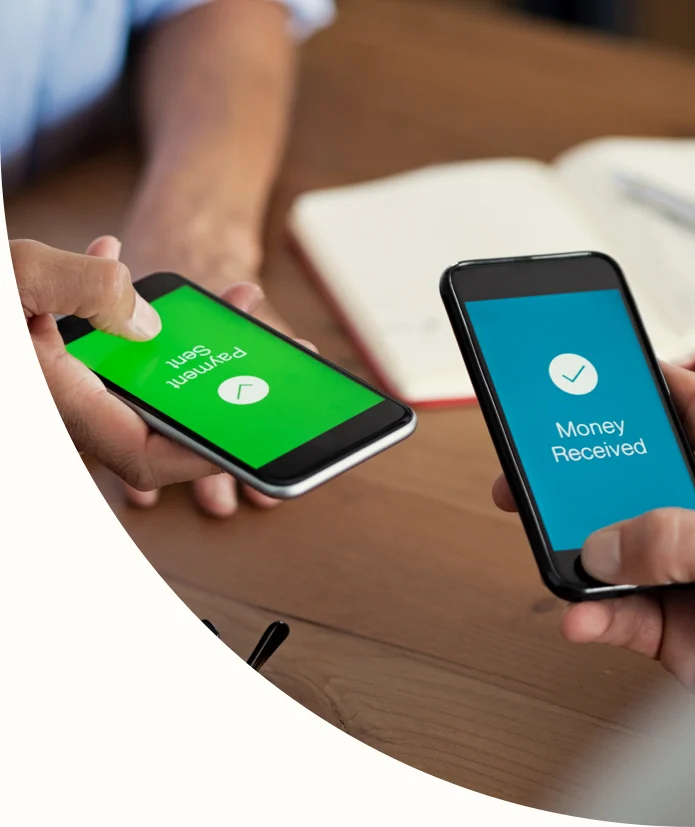

Digital payments – especially instant payments – are reaching ubiquity. Consumers and businesses now expect money to move as fast as information. Many countries have built real-time payment systems: for example, UK’s Faster Payments handles 5.9 billion transactions a year, and the U.S. has rolled out FedNow and private real-time networks. Globally, an estimated 266 billion real-time transactions occurred in 2023, with forecasts suggesting that could more than double to 575 billion by 2028. By 2026, real-time settlement will be the norm for most transfers – from peer‑to‑peer payments to B2B invoicing – instead of weekend‑batch delays.

Why it matters: Faster payments improve cash flow and open new use cases. Businesses can move funds instantly for liquidity management, and consumers won’t have to wait days for transfers. For instance, in 2024 a corporate executed a $10 million liquidity transfer over a real-time rail, demonstrating that these systems can handle institutional volumes. We expect banks and payment providers to upgrade legacy systems (often via cloud‑based hubs) to support ISO 20022 messaging and instant settlement. This trend also underpins many fintech innovations: buy‑now‑pay‑later instalments, embedded payments at point-of-sale, and even programmable payments in metaverse platforms assume real-time rails. By 2026, customers worldwide will routinely send money instantaneously through apps and digital wallets, and cross-border payments will increasingly piggyback on these real-time networks (especially as CBDCs and stablecoins come online).

Embedded finance – the seamless integration of financial services into non‑financial platforms – is transitioning from novelty to norm. Whether it’s a retailer offering instant credit at checkout, a ride‑share app providing driver lending, or an accounting software automatically managing a business’s cash account, more companies are embedding banking, payments, lending or insurance into their user experience. Analysts project the embedded finance sector will reach $7.2 trillion by 2030. Banks are responding: for example, J.P. Morgan and others have launched modular Banking-as-a-Service (BaaS) platforms that let e‑commerce sites or marketplaces plug in financial services via APIs.

Why it matters: Embedded finance breaks down silos and creates new revenue channels. By 2026, any business with customers online could become a fintech provider. Merchants can offer point-of-sale financing or quick deposits without redirecting users to a bank – simplifying workflows and boosting sales. It also brings financial access to underserved customers (for instance, gig workers who can get instant pay advances through their work platform). From the financial institutions’ perspective, partnering via BaaS offers a way to reach new customers with lower distribution costs. As a result, we expect embedded finance to be a default feature of digital services – for example, a dating app might automatically verify a user’s ID for payments, or a subscription service might include integrated saving/spending accounts. By 2026 embedded finance will redefine what a “bank” is: banks will increasingly be the invisible plumbing behind everyday apps.

Open banking – giving third parties secure API access to customer banking data with consent – is expanding into a broader “open finance” agenda. As of 2024 the UK had 10 million active open‑banking users, and global usage is growing rapidly (Statista predicted nearly 64 million open-banking users by 2024 Early open banking use cases (like account aggregation and simple payment initiation) are now giving way to more complex services. In 2026, regulators and industry groups aim to extend open finance to include mortgages, pensions, investments and insurance data, giving customers a holistic view of their financial lives.

Why it matters: Open finance will shift the power toward consumers. Customers could, for example, allow an app to view their entire financial picture – salary, savings, investments, loans and even loyalty accounts – in one place. This enables smarter advice and better deals. For instance, a personal finance app could analyse all of a user’s spending and debts to recommend a consolidated debt product or suggest tax-advantaged investments. Banks and fintechs will be challenged to innovate: the FCA in the UK plans to issue an open finance roadmap by 2026. We expect a wave of new services (e.g. instant pre‑approved loans, AI budgeting) leveraging open data. However, this also raises data security and privacy challenges, so robust APIs and consent frameworks will be key.

Neobanks – digital‑only challenger banks without physical branches – will continue to proliferate. These fintech banks offer banking services entirely through apps and have attracted hundreds of millions of customers worldwide. In 2021 neobanks already had 145 million customers globally, and that is expected to surge to around 360 million by 2026. Major players like Chime (US), Monzo (UK), N26 (Europe) and KakaoBank (Korea) have scaled rapidly by catering to tech‑savvy or underserved demographics with low fees and intuitive interfaces.

Why it matters: Neobanks pressure traditional banks to modernize and innovate. Customers – especially younger ones – increasingly prefer app‑based banking experiences. As neobanks accumulate capital and user bases, we expect consolidation: either the biggest neobanks will grow globally or traditional banks will acquire/sponsor them (as JPMorgan did with the online bank Chase NetBank). By 2026, we will see more bundled “fintech ecosystems” (banking plus insurance and investing under one digital roof), and premium banking apps with AI advisors and lifestyle integrations. However, margins in basic banking are thin, so successful neobanks will diversify into lending, wealthtech or B2B services. In sum, challenger banks will help make finance more user‑centric and push incumbents to invest in their digital platforms.

Regulatory technology (RegTech) will shift from niche to mainstream. As regulatory regimes become more complex globally, financial firms must invest in technology not just to check boxes but to enable growth. The EU’s Digital Operational Resilience Act (DORA, effective 2025) and upcoming EU/UK payment regulations (PSD3) are requiring banks and fintechs to overhaul IT governance, risk management and fraud monitoring. In practice, this means more use of AI‑driven surveillance, digital identity checks and continuous transaction monitoring. For example, a recent industry survey noted that rising fraud has prompted banks to adopt advanced identity verification tools (biometrics, liveness checks) for AML and KYC.

Why it matters: 2026 will see compliance and innovation merging. Compliance will be built into systems by design (e.g. “audit trails” in cloud platforms, automated fraud alerts) rather than bolted on. Demand for RegTech software will rise – one study shows companies are treating compliance infrastructure as a foundation for growth. FinTechs will partner with specialist regtech firms for solutions like real‑time risk dashboards and API‑based reporting. In short, regulation will drive innovation: firms that proactively embed compliance tech will unlock new markets (for instance, enabling cross‑border services by satisfying multiple jurisdictions). Conversely, any startup that underestimates regulatory timelines will struggle. By 2026, robust automation for reporting, risk and data-sharing will be table stakes for any scalable fintech.

Insurance technology (InsurTech) continues to transform the insurance industry. Key trends include AI‑powered underwriting (using data analytics for faster risk assessment), automated claims processing, and new product models (usage-based and on‑demand coverage). The InsurTech sector is forecast to grow strongly: one estimate puts the insurtech market at over $20 billion by 2026. Many insurers have already embraced technology – for example, 82% of insurers reported using AI in claims processing by 2025, which speeds up payouts and fraud detection.

Why it matters: By 2026, insurance will be faster and more personalized. Telematics and IoT devices (like smart home sensors or car gadgets) will feed real‑time data to insurers, enabling dynamic pricing and instant claims. Drones and satellite imagery will automate inspections after disasters. On the consumer side, chatbots and AI will help buyers find tailored insurance bundles (health, auto, property) in minutes. InsurTech also opens finance to underserved segments (micro‑insurance for gig workers, climate-risk cover for farmers). As InsurTech solutions cut costs and improve customer experience, traditional insurers will partner with or acquire fintech startups – similar to banking – to avoid being left behind. Overall, expect 2026 insurance to be much more automated, data-driven and customer‑centric thanks to InsurTech advances.

Environmental, Social and Governance (ESG) considerations are reshaping finance. Investors and consumers increasingly demand that financial services be sustainable. In 2025, global net flows into sustainable funds exceeded $4.9 billion in Q2 alone and governments are enacting climate disclosure rules (for example, mandatory reporting under the EU CSRD since 2024). FinTechs are responding: many challenger banks and payment providers now pledge net-zero operations and offer “green” products (e.g. credit cards that offset carbon). Digital payments have an ecological advantage over cash (less material waste) and players are highlighting this in marketing.

Why it matters: Sustainable finance won’t be a fringe trend in 2026 – it will be mainstream. FinTech platforms will integrate carbon tracking: for instance, an app may show the carbon footprint of each transaction, or nudge customers to switch spending toward sustainable options. Wealthtech robo‑advisors will automatically build ESG‑scored portfolios. On the lending side, banks might reward borrowers for meeting green targets. FinTech firms that ignore ESG risk reputational damage; those that lead in transparency and green innovation may win loyalty. In short, sustainability will be a baseline expectation: banks and fintechs will compete on green metrics as well as fees, and technology (AI for ESG analytics, blockchain for transparent reporting) will underpin it.

As finance goes digital, security is paramount. Cybercrime and data breaches will remain a critical risk in 2026, driving continued investment in cybersecurity technologies. At the same time, quantum computing is on the horizon. Quantum computers could one day crack current encryption schemes, so financial institutions are preparing by adopting quantum‑resistant cryptography. In 2024 NIST issued the first post‑quantum crypto standards, and the global market for quantum-safe security is expected to reach hundreds of billions.

Why it matters: By 2026, banks and fintechs will strengthen defenses on two fronts. First, they will adopt advanced tools – for example, AI‑driven fraud detection (spotting anomalous transactions in real time) and biometric authentication (fingerprints, facial scans) to protect accounts. Regulations like DORA also force firms to build resilience (rapid recovery from cyberattacks). Second, institutions will begin upgrading encryption to quantum-safe algorithms (a regulatory push may even mandate this, given the stakes). In practice, customers will see enhanced security: multi‑factor logins become default, and less data is stored in plain form. Cybersecurity will be a hot topic at boardrooms and tech stacks: firms that fail to keep up (or suffer a major breach) risk losing trust. Hence by 2026, security and compliance will be baked into the innovation roadmap for any fintech.

Technology is transforming wealth management. Robo-advisors – automated, algorithmic investment platforms – have made basic financial advice accessible to millions at low cost. In 2025 robo-advisors globally managed over $1 trillion in assets, and projections suggest this could rise to $2.06 trillion by 2025. The robo‑advisor market (in terms of revenue and AUM) is expected to grow rapidly through the decade (one source forecasts ~10–15% CAGR). More broadly, wealthtech encompasses digital platforms for trading, goal‑based planning, fractional share investing, social trading and more.

Why it matters: By 2026, digital wealth management will be far more widespread and personalized. Even people with modest savings will have access to AI‑driven portfolio optimization and real-time financial planning. Hybrid models (combining robo‑algorithms with human advisors) are also gaining ground – wealth managers use AI tools to augment advice. Younger generations in particular are moving online: 75% of robo users in 2025 were Millennials/Gen Z We expect established firms to partner with or acquire robo‑platforms, and incumbents to launch their own low‑fee digital offerings. The result is democratization of investing: things like automated tax-loss harvesting, ESG‑screened portfolios and 24/7 cryptocurrency trading will be built into mainstream wealth services by 2026.

Cross-border payments have long been slow and expensive, but that is changing. New infrastructures (like blockchain networks, cross‑currency “sleeve” services, and Central Bank Digital Currencies) will drive major improvements by 2026. Already, global real-time rails cover more than 80 jurisdictions (about 95% of world GDP). Industry projects nearly 575 billion real-time transactions by 2028, implying much more cross-border traffic will be near-instant. Additionally, blockchain solutions (for example, IBM’s World Wire) are being used in regions with underdeveloped banking.

Why it matters: Faster and cheaper international transfers will unlock global commerce. Migrant workers will send remittances home in seconds instead of days, often at fees near zero. Businesses will pay overseas suppliers instantly and with real-time visibility of funds. Financial institutions will leverage networks of local accounts (and digital assets) to minimize foreign exchange costs. By 2026 we could see major economies launch interoperable payment systems – for instance, connecting a digital yuan network with FedNow for seamless China-US transfers. In sum, cross-border money will act more like domestic payments, underpinning trade and inclusion in emerging markets. (Notably, if CBDCs become widespread, they too may serve as a bridge currency for remittances.)

Alternative lending is booming, with Buy Now, Pay Later (BNPL) a prime example. BNPL lets consumers split purchases into interest-free instalments at checkout. This model has exploded: globally BNPL transactions are projected to reach about $576 billion by 2026, up from $120 billion in 2021. Beyond consumer BNPL, fintech is offering new credit models such as peer-to-peer (P2P) lending, microloans, and community finance platforms. For example, some apps use alternative data (like phone bills or online activity) to extend micro‑credit to people without traditional credit histories.

Why it matters: By 2026, flexible credit will be embedded into more purchases and services. BNPL in particular is spilling from e‑commerce into physical retail and even B2B purchases. It poses a challenge to traditional banks (retailers and tech firms capturing lucrative credit relationships), but also an opportunity to serve underbanked consumers. Regulators are stepping in (new rules on customer affordability checks are likely), which will shape responsible growth. Altogether, expect credit decisions to become quicker and more granular (instant micro-loans at point-of-sale), and for more specialized lenders to emerge – everything from buy-now-pay-later for business software to subscription‑based financing for solar panels, for instance.

Central Bank Digital Currencies will be a major focus by 2026. Over 130 countries are researching or piloting CBDCs, with a handful (China, the Bahamas, Nigeria etc.) already issuing them. Looking ahead, major economies like the UK, Eurozone and Japan may formally launch retail CBDCs. For example, the Bank of England’s digital pound consultations have drawn tens of thousands of responses, and the digital yuan project remains the world’s largest CBDC pilot.

Why it matters: A widely adopted CBDC could reshape payments. A digital pound or euro would offer 24/7 settlement in fiat with privacy protections built in. Importantly, CBDCs are expected to improve cross-border transfers by acting as a bridge currency (for instance, two central banks could operate a joint digital clearing system). By 2026, even if full retail CBDCs are not launched everywhere, we expect central banks to clarify frameworks and enable wholesale/ interbank digital currency projects. Commercial banks will also adapt – some will handle CBDC distribution to customers. Overall, CBDCs will accelerate existing trends (like instant settlement) and could spur innovations like programmable money (automatic smart contracts for taxes or benefits).

Fintech is exploding in emerging economies, often leapfrogging legacy infrastructure. Asia-Pacific leads in growth – for example, mobile payments and e‑wallet adoption in China, India and Southeast Asia far outpace older markets. Africa has its own success stories: Kenya’s M-Pesa showed how mobile finance can serve millions without bank accounts. Latin America’s fintech sector is also growing quickly, as digital banks target the unbanked. By 2026, we expect emerging markets to constitute a much larger share of global fintech activity.

Why it matters: Financial inclusion is greatest where traditional banking is weakest. Fintech in emerging markets often means simple mobile money, micro‑insurance, and P2P lending for entrepreneurs. These innovations help drive GDP growth and reduce poverty. Moreover, mature fintech hubs (US/EU) are looking to partner or invest in developing regions. As smartphone and internet penetration climbs, even rural users can access sophisticated services through apps. We anticipate significant VC investment in emerging market fintech by 2026, focusing on remittances, SME lending and digital identity solutions. In short, fintech in 2026 won’t be confined to Silicon Valley – it will thrive wherever there is unmet demand for financial services.

Secure digital identity will be a cornerstone of future finance. Banks and fintechs are moving beyond passwords towards multifactor and biometric verification. In 2025, rising fraud pressures led many institutions to adopt more robust ID checks (including facial recognition and AI‑driven anomaly detection). Innovations in this space include digital ID apps (some countries now offer government‑issued e‑IDs) and interoperable identity platforms.

Why it matters: By 2026, seamless identity verification will enable faster onboarding and reduce fraud. Instead of filling endless forms, users may verify their identity once (via a smartphone scan) and then gain instant access to any participating financial service. Improved KYC (know-your-customer) also expands the addressable market: it allows institutions to onboard customers from multiple countries or segments (e.g. gig workers) without heavy paperwork. Privacy-preserving tech (like zero‑knowledge proofs) will play a role, ensuring compliance without exposing unnecessary personal data. Ultimately, a trusted digital identity layer will power many fintech services, from opening an account in seconds to preventing account takeovers.

Personalization will be a defining feature of finance by 2026. Customers increasingly expect their bank or app to understand their unique needs. Surveys show ~84% of customers would switch banks for timely, relevant advice, and 74% want proactive, personalized insights from their financial provider. Fintechs are using AI to meet this demand: data analytics are being applied to spending habits, goals and life events to tailor product offers and alerts.

Why it matters: Personalization drives loyalty and financial well‑being. For example, an app might detect the user’s payday and automatically suggest transferring part of the salary to savings. Or it might flag unusual spending and prompt budgeting advice. Wealth apps will offer tailored portfolio recommendations based on individual risk profiles and even ESG preferences. Behind the scenes, banks are making personalization a priority: by 2025, about 35% of banks listed data-driven engagement as a top strategic goal. In 2026, we expect this trend to bear fruit – customers will see banking interfaces and alerts that feel almost customized, blurring the line between fintech and personal financial advisor. Strong personalization, enabled by AI, will thus be a key differentiator in the market.

The Internet of Things (IoT) – devices talking to each other – will begin to intersect with financial services by 2026. For example, wearable devices (smartwatches, fitness trackers) may be linked to insurance policies: a health insurer could offer reduced premiums if your wearable shows you exercise regularly. Smart home sensors might adjust mortgage or loan rates based on home security features. Payment-enabled IoT devices (smart appliances that automatically order groceries, or in-car systems that pay for tolls) will grow more common.

Why it matters: IoT expands the ecosystem for fintech data and transactions. Connectivity allows finance to be embedded in everyday objects, making financial services more contextual. This trend will also create new data sources for credit and risk assessment (e.g. usage patterns from your car or home). Security and privacy will be challenges – for instance, ensuring payment data from your fridge or car isn’t compromised – but by 2026 standards and encryption will mature. Overall, expect more partnerships between device manufacturers and financial firms: this could mean a bank teaming up with a telematics provider, or a retailer partnering with a smart speaker company to enable voice‑activated payments.

Voice technology and conversational AI are beginning to change how customers interact with finance. Virtual assistants like Siri or Alexa can already answer simple banking queries (“What’s my balance?”) and initiate transfers. In coming years, we expect voice commands and chatbots to become more sophisticated – allowing customers to manage accounts, apply for credit or get investment advice simply by talking to an app or smart speaker.

Why it matters: By 2026, a portion of banking will be “hands‑free.” Conversational interfaces make services more accessible (for elderly or disabled users, or just people on the go). Banks are developing digital avatars and voice agents to handle routine tasks and improve CX. Early adopters report that AI chatbots can resolve common issues 24/7, freeing human staff for complex queries. In practice, you might say “Alexa, transfer £100 to my electricity bill” or “Hey BankBot, what are my spending trends this month?”, and the system will reply with real-time actions. While still emerging, voice banking is likely to be a polished offering by 2026, raising the bar for convenient service.

Data privacy will continue to be a focus as finance integrates with technology. Customers are increasingly aware of how their data is used, and regulations like GDPR (Europe) or CPRA (US) force fintechs to be transparent. In parallel, open APIs (as discussed in open banking) will turn into more general open finance platforms. By 2026, we expect banking platforms to evolve – offering not just data, but modular services (payments, lending, KYC) accessible to certified partners. These APIs will be governed by strict privacy standards: for example, tech solutions for data anonymisation and user consent management will be commonplace.

Why it matters: Security and privacy are non-negotiable. Firms will need to balance personalization (trend 19) with privacy. We anticipate technologies like homomorphic encryption or secure multi-party computation to allow data use without exposing raw info. On the platform side, banks will treat APIs as products – accelerating partnerships. For fintechs and developers, open platforms will lower barriers: a startup could plug into an API for instant KYC, instant payroll, or instant crypto exchange, without building complex infrastructure. This open-API ecosystem – underpinned by strong privacy controls – will create a rich marketplace of financial services by 2026.

2026 will likely see continued M&A and consolidation in fintech. The fintech sector is maturing, and economic pressures have trimmed loose startups: venture funding fell 12% in 2024 and only about half of major fintechs are profitable. In this environment, established players are acquiring or partnering with fintech innovators. For example, 150 acquisitions by traditional banks occurred from 2014–2024. We expect this consolidation to accelerate as banks prefer to buy proven tech (and customer bases) rather than build from scratch.

Why it matters: Consolidation means fewer but stronger fintech brands. Customers will see traditional banks offering “fintech-like” services (often via the technology acquired) and challengers focusing deeper on niches. Partnerships will also grow: banks may give fintechs access to customers and capital, while fintechs supply agile tech or data analytics. Regulators will scrutinise big deals to ensure competition, but overall the trend favors integration of new technologies into incumbents. By 2026, we may see banking-as-a-service become dominant: some fintechs will pivot to B2B models, providing embedded services to banks and platforms rather than competing head-on.

New payment methods and digital asset forms are emerging. For instance, some luxury retailers and airlines now accept cryptocurrency (e.g. Bitcoin, Ether) alongside cash; we expect this to grow as crypto regulation clears up. Non‑fungible tokens (NFTs), while often associated with art, are being explored for finance – e.g. tokenizing ownership of a loan or insurance contract on an NFT. Centralized apps (like stablecoin wallets) may also integrate novel payment flows (buying a coffee with a loyalty token, etc.).

Why it matters: These technologies will mostly underlie more conventional services by 2026. Crypto payments might become a seamless option in wallets, especially where credit cards are less common. Financial innovation labs will experiment with “programmable money” (smart contracts that release funds when conditions are met). The key point is that finance will remain at the cutting edge of digital innovation. For example, by 2026 a business could automatically pay customs duties in digital currency upon crossing a border, cutting paperwork. While not mass‑market yet, these emerging payment forms will exist in parallel and expand options for tech‑savvy users.

While we discussed ESG broadly, we note another trend: finance guided by ethical and social goals. In 2026 this means not just environmental, but financial inclusion and ethical lending. Fintechs will offer products like “green bonds”, impact‑investment robo‑portfolios, and social loan programs (e.g. microcredits for underserved communities). RegTech will also monitor non‑financial metrics (like treating customers fairly).

Why it matters: Customers and investors increasingly reward transparency and purpose. FinTechs that embed ethical standards (for example, limiting data use, or measuring social impact of loans) may find a competitive edge. This trend also aligns with regulation: governments may require banks to show they serve all parts of society. By 2026, we expect some fintechs to differentiate by mission – for instance, a mobile bank that donates a portion of fees to sustainable causes, or an investment app that screens out controversial industries. Ethical finance may not have the most citations in data, but it will inform the values driving fintech innovation.

Fintech continues to reach the previously unbanked. Microfinance apps and mobile banking have brought financial services to remote and low‑income populations. For example, smallholder farmers can use app‑based credit to buy seeds. By 2026, we expect further breakthroughs: AI credit models might lend to gig workers with irregular income, or blockchain platforms could enable peer-to-peer lending in developing markets without going through banks.

Why it matters: Financial inclusion is not just a social good – it represents a huge new market. Expanding credit and insurance to billions more people fuels economic growth. Technology (mobile, biometrics, alternative data) reduces costs for serving these customers. As an example, micro‑insurance (e.g. weather insurance for small farms) delivered via smartphone will become common. In sum, fintech will continue bridging global gaps: payments and financial planning for the 2.5 billion unbanked by 2026 will largely be managed by smartphones and apps, rather than brick‑and‑mortar branches.

Conclusion: The fintech landscape in 2026 will be defined by integration and acceleration. Technologies like AI, blockchain and cloud native architecture will become foundational, embedding seamlessly into every financial product. Speed – of transactions, of data, of decision‑making – will be the expectation. Regulation, far from stifling innovation, will guide and legitimize it (for example through DORA, PSD3, MiCA or CBDC frameworks). Ultimately, customers will benefit from more personalised, inclusive and efficient financial services. The winners will be those who anticipate these trends and build trustworthy, agile platforms – combining advanced technology with sound risk management and a human‑centred approach. As one fintech strategist put it, 2026 is not about isolated innovations but about “reshaping the core of financial services” – a future where finance works smarter, faster and more fairly for everyone.

Fintech Business Asia, a business of FinTech Business Review

© 2026 FinTech Business Review. All Rights Reserved.